Often, founders of companies simply hold common stock while the company investors hold preferred stock, which comes with certain rights and preferences.

Let’s say that you started a company and maybe even got your first round of funding. Things are going well, you got traction, MVP, and revenue. Let’s say that things are going really well and you end up doing a Series A round. Now you have two classes of shares in your cap table: Series A and Common.

Well, let’s say things are going extraordinarily well and you have reached millions in revenue, growth rates are through the roof, and the company is getting a lot of attention. Let’s say you are the founder and get an offer from an outside investor to buy common.

Good deal right? You get liquidity and are sharing in the company’s success. Sorta. The only factor that is problematic is that this will raise the price of your common stock and in turn, the options you are granting employees. This screws over your employees, causes less liquidity, harder for it to be in the money, larger tax burden. I have seen this happen many times.

So how do you avoid this, level the playing field a little, and still give liquidity to founders? Let me explain Series FF stock below.

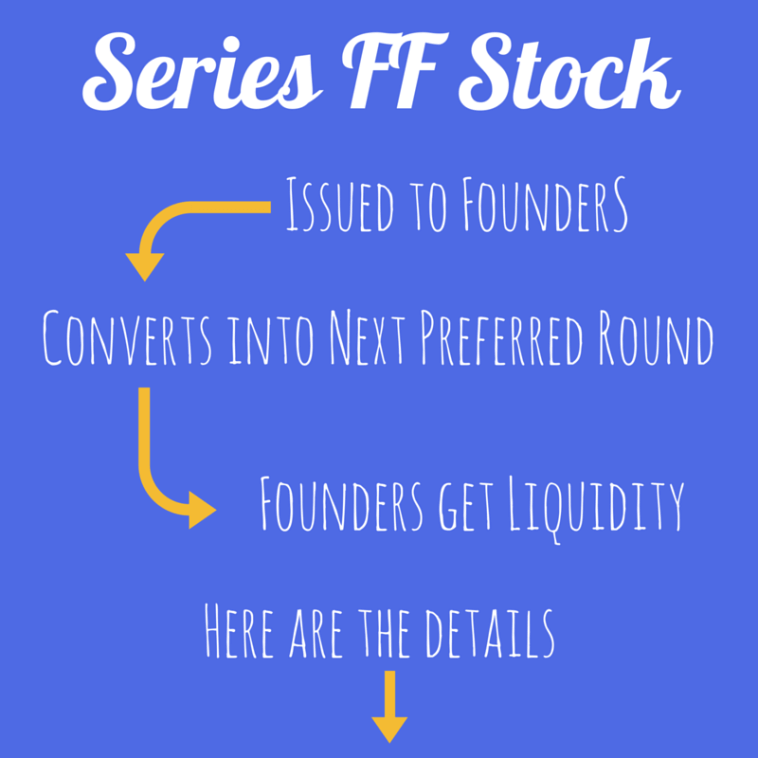

What is Series FF stock?

Series FF stock is a separate class of preferred stock that is issued to founders at the time of incorporation but is basically identical to common except that it is convertible to into shares of the into shares of the series of preferred stock issued to investors in a later financing round (Series A) and sold as part of that round.

So for example, if a VC invests $20 million in a Series A round, it might acquire $17 million in newly issued Series A shares and buy $3 million worth of Series FF shares that convert to Series A from the founder(s). The Board will usually place a limit on how much of a founder’s interest can be sold, to make sure he or she still has enough skin in the game, so to speak.

Below are some things to keep in mind about Series FF stock:

Pricing of Series FF stock is complicated

Generally, stock should be issued at fair market value (otherwise, there may be deemed income from the company to the founder). If the Series FF is not issued at initial incorporation, then issuing the Series FF stock at a later point in time will require the founders to pay more than a nominal amount to purchase the shares.

As I will describe in a later post, founders’ stock is typically issued at a very nominal price per share, such as $0.001, so the company may initially issue 10,000,000 shares for $1000.

Series FF stock has liquidation factors to consider

If the Series FF is issued immediately prior to the Series A financing, then the price per share of the Series FF probably should be at least the same as the Series A. In some respects, the Series FF may be more valuable than the Series A in the future if it can convert into a later round of preferred stock with a liquidation preference greater than the Series A.

On the other hand, there is a significant risk that the holder never receives liquidity because the board might not allow a conversion to occur (or investors may not be willing to purchase).

Potential higher legal fees

Legal fees incurred in issuing Series FF may be higher. This is because the Series FF receives some amount of custom drafting and tweaking compared to a typical incorporation.

In addition, many attorneys are not familiar with the concept and there are costs incurred in “reinventing the wheel” and getting everyone comfortable. The additional costs involved in setting up the Series FF may be wasted if the future board does not allow the founders to obtain liquidity.

Timing impacts equity financing

It is unclear whether venture funds are willing to allow founders to sell a portion of their stock in connection with venture financing. Implementing the Series FF before equity financing sends a message to potential investors that the founders want liquidity in connection with equity financing.

This may not be a good thing to mention when looking for early rounds of financing. However, venture funds may be willing to allow founders to sell in the following situations:

- The venture fund has to agree to it because there are multiple terms sheets in a competitive deal.

- The company is doing well (i.e. valuations above $100M and nearing an IPO) and the founders would rather sell the company than wait longer for liquidity.

Stock pricing differences to consider

Other mechanisms exist to allow founders to receive liquidity in connection with venture financing. Companies can repurchase founders’ common stock for cash, subject to various limitations. The main issue that the Series FF solves is the price difference between preferred and common stock.

If common stock is repurchased by the company at the same price as preferred stock is being sold to investors, then the fair market value of the common stock for option pricing purposes probably should be the preferred stock price.

However, in a company nearing an IPO, the common stock FMV will likely be very close to the preferred stock price anyway. Therefore, the Series FF stock probably only incrementally solves a situation where founders want liquidity and want to preserve a significant price difference between the common stock and preferred stock in early-stage venture financing.

Let’s talk

Schedule an intro call to learn about why MeldVal is important for your business. Or have any questions? We’re here to help.

Contact us