Compliance, Fundraising

Why Independence Matters - 409A Valuations & Safe Harbor

By Dan Eyman

October 10, 2018

If you are planning to offer stock to employees, advisors, contractor or any other stakeholder, then you need a safe harbor for 409A valuation. This is the only way to protect your business from being penalized by IRS.

In 2005, IRS introduced 409A as a reliable way of controlling private companies that offer common stock options and other deferred compensation plans. Since stock is treated as deferred compensation, you must get a 409A valuation to determine the strike price. This will ensure that employees buy equity in your firm at a fair market value. That said, you should know that there are dangers of if you are planning to use non-independent valuations firms.

So how do you get yourself protected?

Are there any consequences for non-compliance?

Following IRS ruling 409A , granting at fair market value, is an IRS requirement, and non-compliance usually attracts serious implications. If you offer common stock to your employees as deferred compensation without a proper valuation you are exposing your company and staff to huge financial risks. IRS will penalize your employees if they find out that you did not comply with the valuation standards, and you issued the stock at a price below the fair market value. Here are some of the consequences that the affected employees will face.

– They will be taxed all the issued stock as if it were part of their gross income

– They will pay a penalty of 20%, in addition to the above

– There could be other additional penalties and interest that may be levied on the affected staff

The above situation is definitely not what you want your employees to go through. Besides, It would give your business a bad reputation.

So why is safe harbor important and how you can get it?

Ideally, safe harbor insulates you from persecution. Luckily, IRS has provided avenues for companies to safely offer deferred compensations. If you have a safe harbor, IRS will only reject the valuation if they can prove that it is grossly unreasonable. The burden of proof is with IRS to prove that you are in error. However, this burden of proof is shifted to the company and BOD if don’t have safe harbor. In this case, you are treated as having granted cheap stcok unless you can prove otherwise and defend your strike price.

For the valuation to be treated as safe harbor valuation, it must be done in any of the following ways, but we will focus on the first two.

1. Valuation be done by a qualified third party valuation company

2. Valuation be done internally by a qualified staff

3. Stock be offered through a generally acceptable repurchasing formula

1) Using Internal Value

In this option, the company will appoint a qualified individual from the internal team to conduct the valuation. This can be one of the easiest and cheapest options, but it has several other conditions attached to it. The individual doing the valuation and the company must meet set standards.

The individual appointed to do the valuation must have at least five years’ experience in a field related to valuation. This includes business valuation, private equity, investment banking, secured lending, or financial accounting. This can be tricky because there is room for subjectivity. IRS, upon its discretion, may determine that the individual who did the valuation did not meet the required standards. Further, what we have seen to often is the internal valuation results in values way to high or just plane wrong. Experience matters.

Moreover, a company can only use this option if it can meet the following requirements:

– It is a private company

– Has no publicly traded stock

– Is less than ten years old

– Has no stock that is considered as a call, put, or similar derivative

2) Appointing a Third Party Firm

While this may be the most expensive option, it is also the safest. The only condition is that the firm should follow consistent methodologies in the valuation. So, it is important to supply the firm with all the necessary information to carry out the valuation. The information includes the following.

With the requested information, a qualified firm can do a reasonable valuation. In some instance, a third party firm may arrive at a favorable fair market value without going too low to raise alarm.

Today, there are several 409A cap table software firms, and this has helped to bring down valuation charges. This is why nearly half of startups choose this option. The advantage of working with a third party firm is that you get double protection. Most firms will be interested in saving their reputation, so they are more likely to protect you. Moreover, the burden of proof lies with IRS.

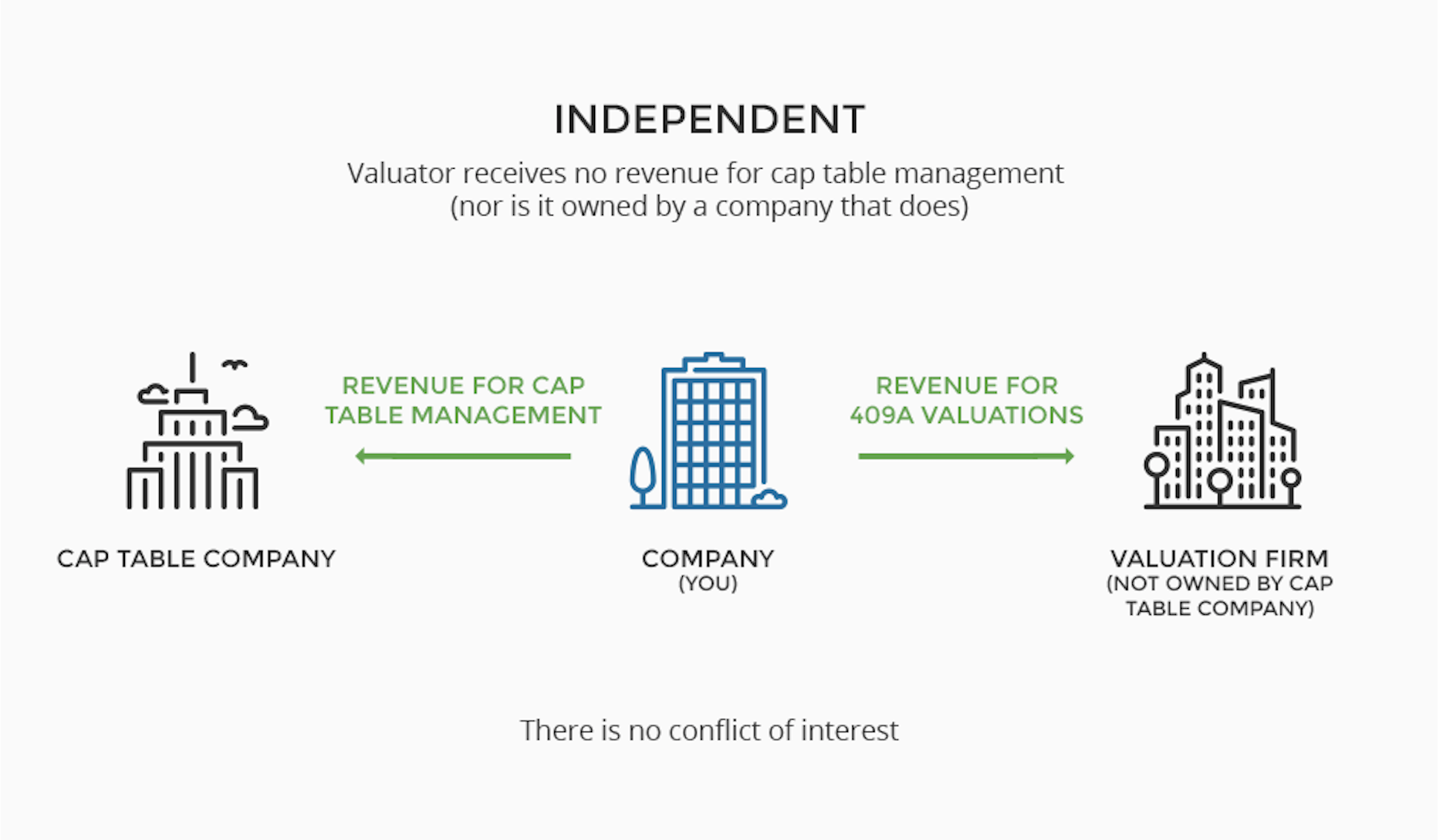

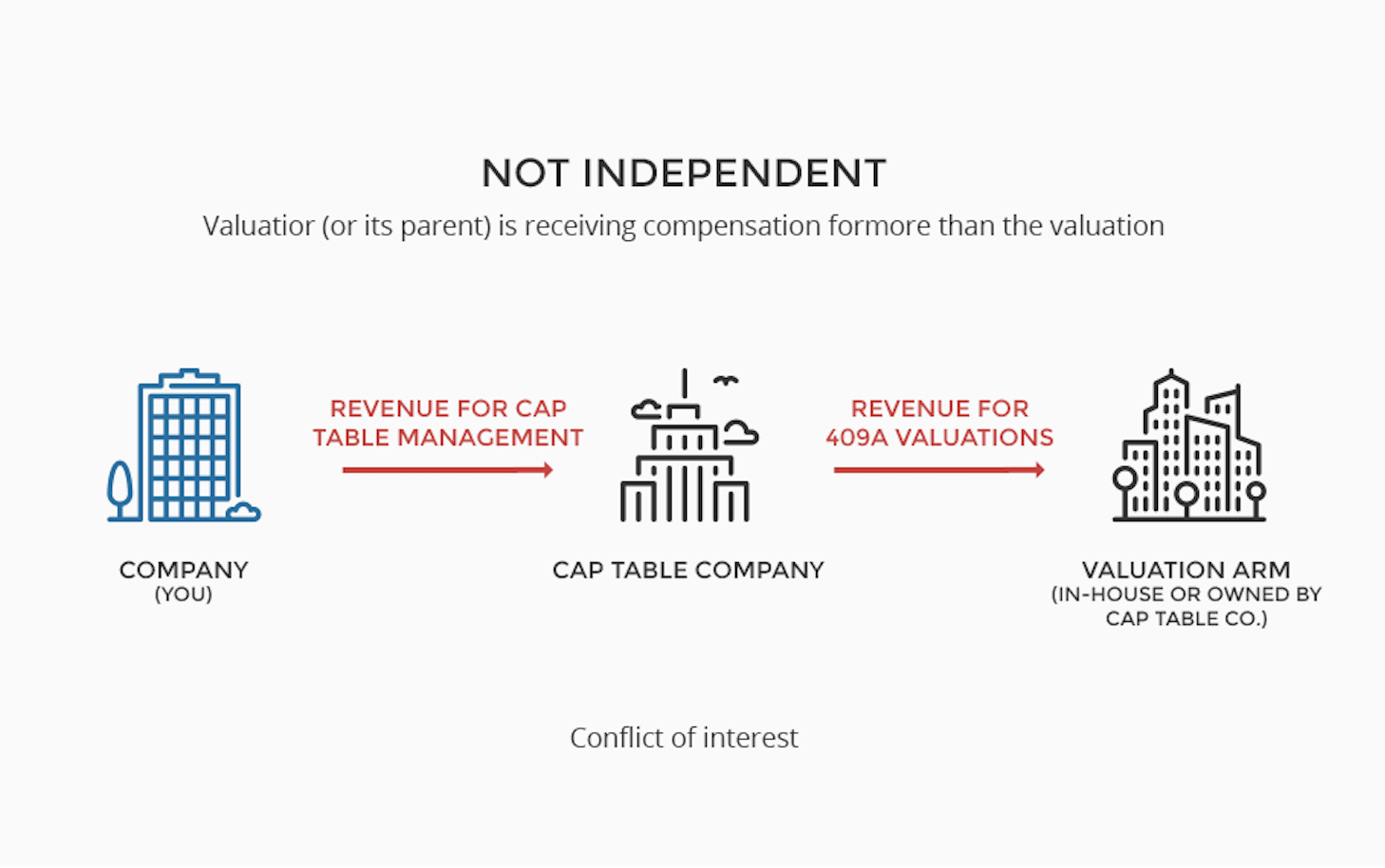

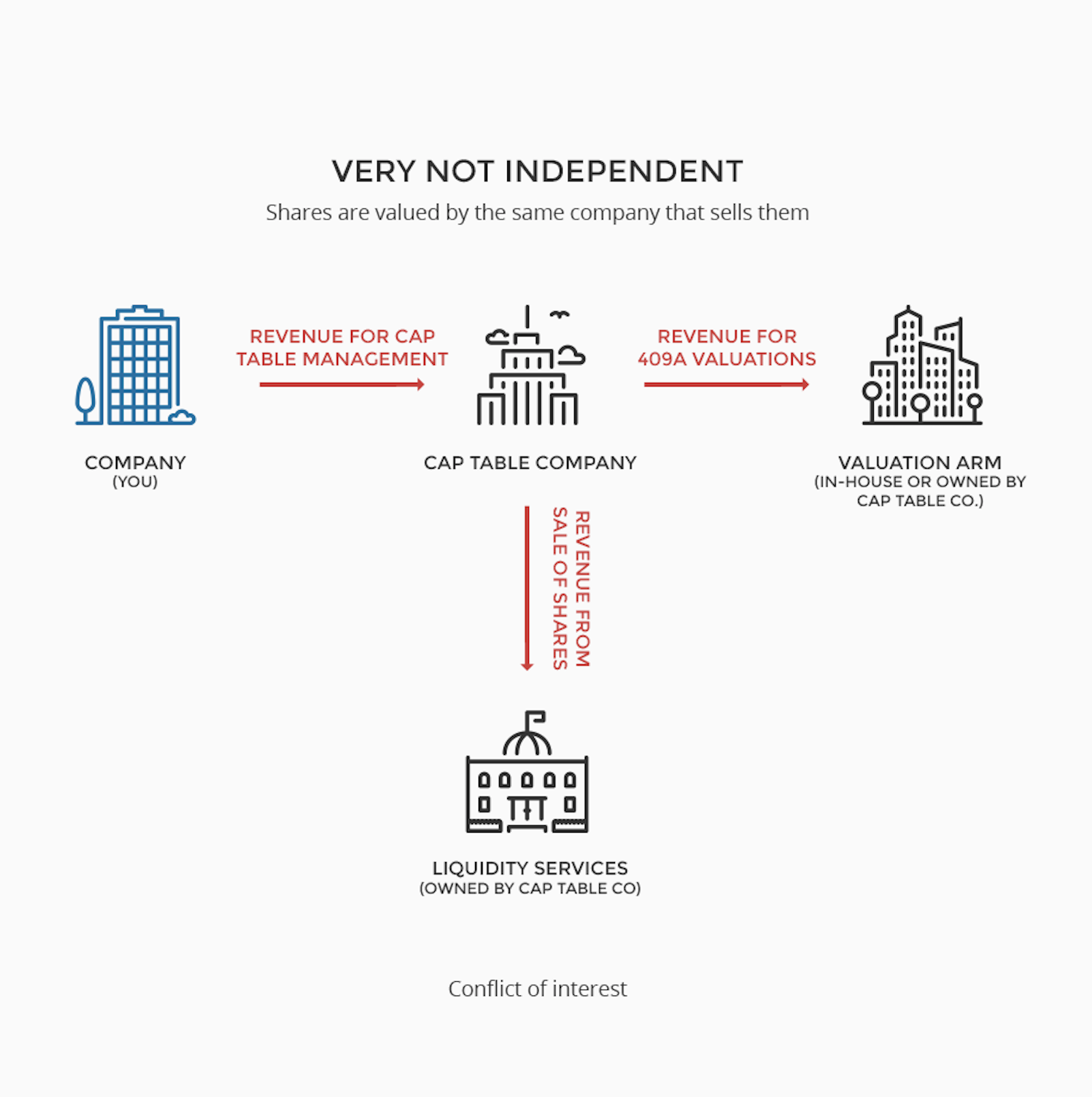

The Dangers of Working with Non-independent Valuation Firms

For a company to be deemed as independent, in IRS context, it should only provide you with valuation services. Some companies may be tempted to register a separate LLC company to handle valuations but the conflict of interest is their regardless.

To qualify for a safe harbor, valuers must be seen to be independent. They should also employ objective judgment in arriving at their conclusion. In this case, there should not be any conflict of interest, and valuation should be based on merit, free of bias. Therefore, if a valuation company receives other forms of income that are not related to valuation from your company, then that amounts to a conflict of interest. There is even a bigger conflict of interest if the valuation firm offers liquidity to the same shares it is valuing.

Legally, conflict of interest indicates the presence of economic benefit. In that case, IRS requires valuation firms to declare that there have no relations with their clients. On top of this, they should also attest that the compensation is not based on the results they deliver. The bottom line is that you will not achieve safe harbor if is there is a conflict of interest.

So, when can you say you have fully achieved safe harbor?

If your valuation has respected all the requirements for achieving a safe harbor, then you are almost guaranteed of protection, but you are not off the hook yet. The following caveats need to be taken into consideration.

– If there is material change that might have a direct impact on the value of the company, then the valuation will become invalid.

– The valuation is valid for 1 year, so if you are issuing additional shares after 12 months, then you should do a new valuation.

– IRS still has room to determine if the valuation was grossly unreasonable

It may seem like a daunting task to do 409A valuation the right way, but it is worth the effort because the consequences for violations are severe. Remember that safe harbor is the best way to protect yourself against harsh penalties.

Let’s talk

Schedule an intro call to learn about why MeldVal is important for your business. Or have any questions? We’re here to help.

Contact us